Are you being taxed without even noticing it?

After closely studying the impact of many countries’ tax systems on their citizens, I was surprised to see that some countries adjust tax exemptions and thresholds for inflation every year, while others simply do not. Terms such as “threshold” or “exemption” may sound harmless and even beneficial to taxpayers. Yet, they can easily be weaponized into a hidden form of tax increase, often referred to as fiscal drag. With this in mind, I explored key examples of this phenomenon, comparing how different countries handle it to help you better understand the impact of these hidden taxes.

Role of Structural Inflation in the Economy

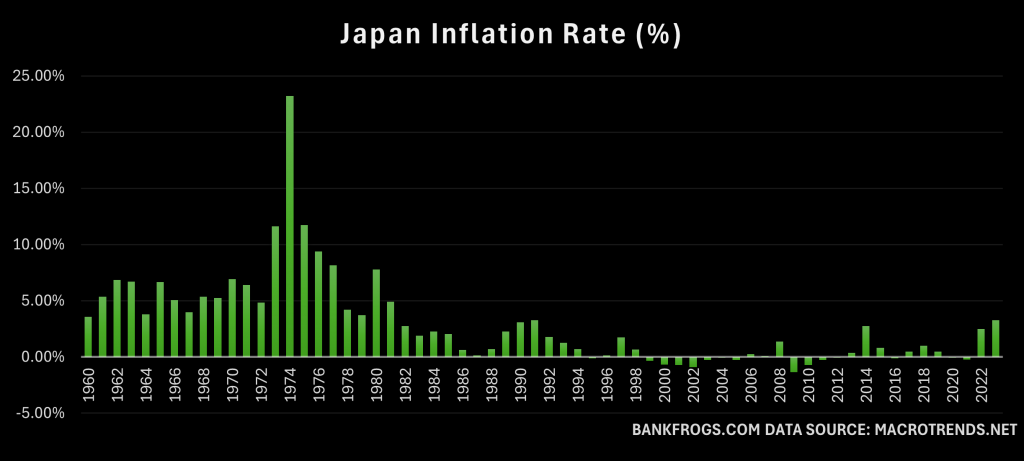

First, do we even need inflation? The US Federal Reserve aims for a 2 percent inflation rate over time to support its objective of “maximum employment and price stability”. An inflation target which has become the norm in most of the developed world. While inflation in the US has often been below this target, too-low inflation can lead to economic stagnation, as it causes expectations for future inflation to fall. This can result in a cycle of declining inflation and lower interest rates, reducing the ability to stimulate the economy during downturns. This has been the case in Japan during the “lost three decades”. It reduces consumer spending, as people delay purchases, and increases the real cost of debt. Businesses invest less, leading to higher unemployment. By accepting structural inflation, some nations have adapted their tax systems to benefit from it.

UK Frozen Tax Thresholds

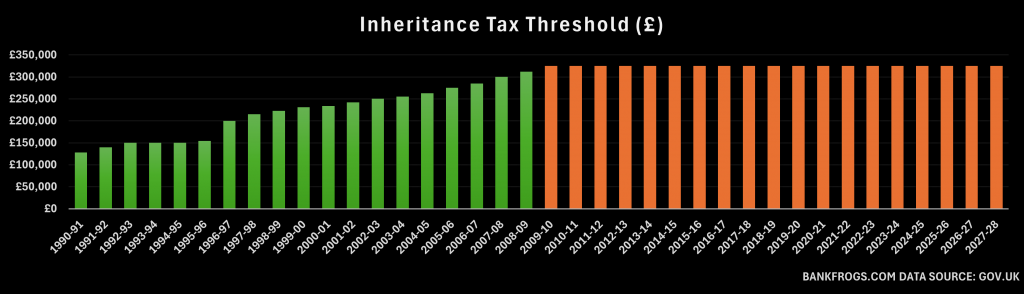

The UK government’s decision to freeze key tax thresholds from 2020 until 2028 represents a form of fiscal drag, a type of stealth tax. This policy effectively increases the tax burden for individuals without raising tax rates directly. The freeze applies to several key tax thresholds, including the income tax Personal Allowance, higher-rate tax threshold, and National Insurance contribution thresholds. These numbers will remain unchanged until at least April 2028. For more details on the UK Tax system see Understanding the City of London Corporation.

Freezing tax thresholds means they do not rise with inflation, even as wages increase. Over time, this pushes more individuals into higher tax brackets, exposing more of their income to higher tax rates. This form of fiscal drag reduces the real value of earnings. People end up taxed on money that has less purchasing power, diminishing the benefits of wage increases and lowering their standard of living. A boiling frog approach to taxation.

Real Financial Impact of the Freeze

The Office for Budget Responsibility has projected the following significant increases in taxpayers by the end of the policy period (2027-28):

- 3.2 million new taxpayers will emerge, representing a 9% increase in the number of taxpayers.

- 2.1 million new taxpayers in the 40% tax bracket, a 47% increase in taxpayers affected.

- 350,000 new marginal rate taxpayers, an almost 50% increase in those paying the highest tax rate.

Looking at the numbers, this stealth tax disproportionately affects middle-income earners. A common trend in non-inflation adjusted systems.

Inflation pushes the income of more taxpayers beyond the frozen thresholds. This was initially expected to raise £29.3 billion annually, or 1.0% of GDP. From a historical perspective, the freeze on the personal allowance takes its real value in 2027-28 back to where it was in 2013-14. Effectively, this is an increasing reliance on fiscal drag to generate revenue without the transparency of a traditional tax rate hike.

Decades Long Freezing in France

In neighboring France, the implementation of frozen tax thresholds has been even more drastic than in the UK Over two decades ago, on January 1st, 2002, the euro replaced the French franc. Despite this shift, the exemptions offered by one of the most popular estate planning strategies for French residents, the French life insurance (assurance-vie), have remained unchanged.

Under the French tax code, each policyholder can pass up to €152,500 per beneficiary, free of French inheritance tax, provided the funds are invested in the policy before the policyholder turns 70. This exemption applies per policyholder and per beneficiary. For example, a married couple with two children can transfer up to €610,000 free of inheritance tax in France.

But why €152,500? This amount corresponds to the now defunct 1 million French francs, a limit that has remained unchanged for decades. The 1999 version of article 990I CGI, set the exemption at 1 million francs, and it has remained the same ever since. However, taking into account the French cumulative inflation rate of approximately 53% since then, the amount should now be closer to €233,000.

This can be added to the base exemption on inheritance per child per person of €100,000, which was reduced and fixed at this amount in 2013. Prior to that, the exemption had been increased annually for a period of time. This value should be closer to €122,000 today if it was adjusted for inflation.

| Exemption | Current Amount | Inflation Adjusted |

| Inheritance for Descendants | €100,000 | €122,000 |

| French Life Insurance | €152,500 | €233,000 |

Backtracking on Exemption Amount Increases

Just as France reduced its inheritance tax exemption from €159,325 to €100,000 in 2013, the US is set to backtrack on its federal estate tax exemption. Currently set at $13.99 million per individual, this exemption is scheduled to decrease in 2026 unless Congress intervenes (which is very likely). If no action is taken, the exemption would revert to around $7 million per person, adjusted for inflation. As a result, many high-net-worth individuals have turned to estate planning strategies taking advantage of the current higher exemption amounts before the reduction takes effect.

Similarly to the US, the Canadian tax system also adjusts most tax brackets and benefits for inflation annually. However, inflation adjustments are not uniform in the US system as many exemptions have long been fixed for years, even decades. This includes the reporting of ‘foreign’ (non-US) accounts using a Report of Foreign Bank and Financial Accounts (FBAR) on Financial Crimes Enforcement Network (FinCEN) Form 114. Unlike the frequently amended Bank Secrecy Act of 1970 and its associated penalties, the original $10,000 FBAR reporting threshold has remained unchanged. The amount set 65 years ago, when President Richard Nixon signed the law, would be equivalent to over $80,000 in today’s dollars.

Fixed Income Tax Thresholds in Inflationary Economies

According to the Tax Foundation, few countries adjust their income tax thresholds for inflation. Out of 160 economies analyzed worldwide, 131 do not make any such adjustments. The remaining countries make regular adjustments, although only nine have explicit rules to adjust their income tax thresholds for inflation.

The eurozone is an interesting case. The European Central Bank has collected data on tax rate adjustments across these countries. The data reveals important fiscal drag, especially in personal income taxes. Most eurozone countries have progressive tax systems, where tax rates increase with income. However, because many of these countries do not adjust the tax brackets for inflation, their systems are vulnerable to fiscal drag. Other taxes, including corporate taxes and social contributions, are less affected as they are either proportional or have limits. Excise taxes, which apply to specific goods or services, are fixed amounts and unaffected by price changes.

Inflation Stonks

Automatically adjusting taxes for inflation benefits taxpayers by preventing tax payments from rising simply due to inflation. However, politicians often hesitate to support these measures as it limits their ability to make discretionary adjustments. Without the flexibility to adjust taxes based on economic conditions or voter preferences, they struggle to present themselves as proactive in managing the national economic policy. Despite the logic and predictability behind automatic adjustments, these types of policies are often difficult to introduce and are overshadowed by more flexible fiscal strategies.

While the fixed tax thresholds may appear as technical adjustments, these act as stealth taxes on taxpayers. By creating fiscal drag, the government can raise revenue while minimizing the visibility of the increase.

Related Posts

Reference

- Liberty Loan poster promoting US government bonds during the Second Liberty Loan of 1917. During the most significant spike in inflation in US history. Featuring the US Treasury Building (1917). Library of Congress Prints & Photographs Division.