Is leaving your country worth the exit tax?

In an increasingly globalized world, the ability to travel freely between countries is one of the key pillars of global mobility. However, for many expatriates, entrepreneurs, and individuals seeking to change their residency status, this freedom can come at a significant financial cost. Exit taxes, imposed on individuals when they renounce their citizenship or leave a country, have become a growing obstacle for those wishing to relocate. Countries including Germany, France, Japan and even the United States have implemented exit tax policies, which can create an important financial dis-incentive for people to leave or even relinquish their nationality. We will explore the implications of exit taxes worldwide, how they affect global mobility, and the potential consequences for those seeking a fresh start abroad.

Recent Exit Tax Updates in Europe

Recent developments in exit tax systems across several European countries have renewed the dialogue about the impact of these taxes on global mobility. As governments tighten regulations to prevent tax avoidance, they are increasingly focusing on assets held when individuals or companies relocate outside their borders. More specifically unrealized capital gains, the difference between the market value and the value at acquisition of these assets. Nations following Germany’s lead have recently expanded the scope of their exit taxes. A wider range of assets are now subject to this levy. For instance, the German exit tax now includes both corporate holdings and private investments. In 2025, one of its most important revision has been the inclusion of self-employment assets in the scope of this tax. Private investors with substantial holdings are also targeted. This includes those with more than €500,000 ($540k) [1] in investment funds or a single exchange traded fund.

The Netherlands has been drawing inspiration from the evolving German tax framework. It is set to introduce its own exit tax measures in 2025. These would target wealthy individuals and entrepreneurs who relocate to low-tax jurisdictions. The tax will likely apply for a defined period following an individual’s departure, potentially extending for up to five years. The objective is to ensure that those who have benefited from the economic environment of the Netherlands continue to contribute fairly to its tax base, even after they have relocated. Norway, also following Germany’s lead, has introduced major reforms to its own exit tax system in the 2025 Norwegian National Budget. Under the new rules, individuals leaving Norway with unrealized capital gains exceeding NOK 3 million (approx. $280k) [1] will be subject to the tax.

In certain cases, individuals can defer exit tax payments by meeting specific conditions or providing collateral. Since 2025, Norway enforces a 12-year rule requiring individuals to pay the exit tax within this period, regardless of whether the assets have been sold. If an individual returns to Norway within this 12-year window and still owns the taxed assets, the exit tax on those assets will be canceled.

The 1st German-Netherlands Corps (1GNC) is a multinational military formation consisting of German and Dutch forces, established to enhance defense cooperation and operational readiness within NATO.

EU Exit Taxes and Fundamental Rights

The issue of exit taxes within the European Union is complex, shaped by a combination of EU regulations, national laws, and principles of global mobility that are essential to the functioning of the Union. Central to this framework is the Anti-Tax Avoidance Directive, which was introduced to address concerns regarding aggressive tax planning by individuals and businesses. It was passed to ensure that profits are taxed where the economic activities generating them take place. This directive forms the basis for many exit tax systems within EU member states. It provides a common framework that seeks to prevent the shifting of taxable assets to low-tax jurisdictions, so as to undermines the collection of higher-tax countries.

At the heart of the EU’s legal system are key principles embedded in foundational documents. These include Article 21 of the Treaty on the Functioning of the European Union and Article 45 of the EU Charter of Fundamental Rights. Both provisions guarantee the freedom of movement for workers and the right to pursue economic activities in any EU member state. They lay the groundwork for the EU’s commitment to promoting the global mobility of individuals and businesses within its borders. Those rights are designed to foster the Union’s goal of creating a common and dynamic internal market.

However, as EU member states implement national exit tax laws, the challenge arises in balancing the need for anti tax avoidance measures with the preservation of these fundamental rights. This tension has led to scrutiny from the European Commission, which has stepped in to address situations where national laws disproportionately limit individual’s ability to relocate across EU borders.

In recent years, the European Commission has raised concerns over Denmark’s exit tax legislation, specifically regarding the taxation of individual shareholdings. The Commission argued that the current law may unnecessarily restrict the free movement of individuals within the EU. While the Danish law was designed to prevent tax avoidance by taxing capital gains in Denmark, the Commission pointed out that it could disproportionately restrict the ability of EU citizens to move freely and pursue economic opportunities in other member states. Although the law targets tax avoidance, it must be balanced with the broader EU framework protecting individual mobility.

As exit tax regulations evolve across the EU, each member state must incorporate these directives into their domestic laws. They must also ensure domestic law does not unintentionally violate individuals’ rights under EU law. The European Commission is closely monitoring these developments, calling on member states to adjust their tax policies when conflicts with EU law arise.

Relocating to a Low-Tax Jurisdiction Outside the EU

The decision between relocating to a low-tax jurisdiction and maintaining mobility within the EU is complex. Exit taxes often deter entrepreneurs and investors from moving. In France, the exit tax has faced criticism for diminishing the country’s economic appeal. It discourages individuals from staying, as many plan their expatriation before reaching tax thresholds or domicile requirements. Although discussions around reform or abolition of the tax continue, no concrete changes have been made. Critics argue that it undermines France’s attractiveness to foreign investors and skilled professionals, especially compared to countries with more favorable tax policies.

Similarly to France, the exit tax rules in Denmark vary based on whether a double tax treaty exists with the destination country. Beyond asset-based exemptions, individuals can apply for a payment deferral under certain conditions, such as providing collateral. This approach is similar to the German system.

Both France and Denmark aim to prevent tax avoidance. However, by factoring in other countries when applying an exit tax, they can create financial incentives that align with the broader EU-wide principle of freedom of movement.

Exit Tax Avoidance Through Short-Term Mobility

Exit taxes usually apply to individuals who have been long-term residents of a country. As a result, many have a financial incentive to remain highly mobile or limit their stay to avoid triggering these taxes.

Multiple European countries impose exit taxes on individuals who have been residents for a set number of years before leaving. In some cases, this period can be as short as six to ten years. Since these taxes typically target unrealized capital gains on specific assets, Individuals with net holdings above certain thresholds are particularly affected. For example, France applies the tax to those with assets over €800,000 ($870k) [1] or company stakes. These measures can result in individuals planning their expatriation around the tax thresholds, either by limiting their time in the country or relocating quickly to avoid the tax.

Spain and France use exit taxes to ensure that individuals who accumulate significant wealth during their residency are taxed on unrealized capital gains when they leave. Spain’s exit tax applies to those who have been tax residents for at least 10 of the previous 15 years and hold assets above certain thresholds. Likewise, France’s tax applies to individuals who have been residents for at least six of the last ten years, focusing on individuals with substantial holdings or business interests.

Other countries, such as Germany and Denmark, impose similar exit taxes provisions, although the specific residency requirements and taxable assets vary. The German exit tax applies to individuals who have been residents for at least seven of the previous twelve years. Denmark applies its exit tax to those who have been fully taxable in the country for at least seven of the last ten years before leaving. Beyond Europe, Japan also has similar minimum residency requirements for an exit tax to apply. It affects individuals having resided in the country for more than five of the past ten years under a more permanent residency status before leaving.

While these taxes aim to prevent tax avoidance, they also create a strong financial incentive for individuals to remain mobile and minimize their exposure.

Tax Assessment and Exemptions

The majority of exit taxes apply on unrealized capital gains upon leaving the country. These taxes are based on the concept of “deemed disposition,” meaning that assets are treated as if they were sold at fair market value on the departure date, even if no actual sale occurs. While exit taxes generally target financial assets including stocks and bonds, each country has its own set of rules, including exempt assets, special cases, and thresholds.

In Denmark, the exit tax applies to unrealized capital gains on various assets, including stocks and bonds. These assets are treated as if they were sold on the departure date, with the tax calculated based on their fair market value. Similarly, France imposes its exit tax on unrealized capital gains held the day before an individual leaves the country. It targets securities such as stocks, bonds, and shares in companies that primarily invest in real estate. However, life insurance policies and direct real estate holdings are exempt. France also offers deferral options for individuals relocating to EU countries or jurisdictions with tax agreements, including the UK. In some cases, this deferral is automatic, allowing individuals to delay the tax payment.

The Spanish exit tax is triggered for residents owning shares or participations in entities valued at over €4 million ($4.3m) [1] or holding a 25% or greater stake in a company valued at over €1 million ($1.1m) [1]. The business ownership aspect is becoming increasingly relevant for entrepreneurs. For instance, Germany’s exit tax targets business owners who hold more than 1% of a company, ensuring the country collects taxes on any potential sale proceeds from the business.

The exit tax in Japan also targets individuals who hold financial assets. These must be worth at least JPY 100 million (approx. $700k) [1] at the time of departure. Strategically selling investment assets to purchase exempt assets, such as artwork or real estate, does not effectively avoid Japanese taxation. The tax is based on the deemed disposition of assets rather than actual sales. Selling assets before departure only results in paying the tax sooner, as it is precipitated by an actual sale.

Similarly, South Africa imposes an exit tax in the form of capital gains tax when individuals cease to be tax residents. The tax is triggered upon a formal change in tax residency. However, personal use items, immovable property located in South Africa, and retirement annuities are exempt. A percentage of the capital gain is added to taxable income, with an annual exclusion available to reduce the taxable gain.

Despite the lack of a formal exit tax, Australia does impose a capital gains tax when individuals cease to be Australian tax residents. Certain assets are deemed sold at market value upon departure, resulting on a the taxation of unrealized gains. However, taxable Australian property, such as real estate, remains subject to capital gains tax regardless of residency status. Canada also imposes a similar “departure tax” on individuals leaving the country. Mimicking other jurisdictions, it taxes unrealized capital gains on worldwide assets at the time of departure, with exceptions for assets such as Canadian real estate and pension plans. Canada also allows individuals to defer payment by providing collateral to the Canada Revenue Agency.

For Australia and Canada, the cost basis of assets is assessed when the individual becomes a tax resident of the country, not when the asset was originally acquired.

An Exit Tax for Tourists?

The Japanese exit tax should not be confused with the International Tourist Tax, a small levy of JPY 1,000 ($7) [1] imposed on all visitors leaving Japan. Introduced in April 2019, the tourist tax is designed to support tourism-related infrastructure and initiatives, for the benefit of future visitors. Unlike the exit tax, the tourist tax applies universally to all travelers, regardless of their residency status or financial holdings.

The Unique United States Exit Tax

The United States has a unique exit tax system that applies when individuals renounce their US citizenship or relinquish their Green Card. This exit tax primarily affects covered expatriates, a classification for individuals who meet at least one of the following criteria: a net worth of $2 million or more on the expatriation date, an average annual net income tax liability exceeding $206,000 (2025 amount adjusted annually) over the past three years, or failure to certify compliance with US tax obligations for the five years prior to expatriation.

The exit tax treats all property as sold at fair market value before expatriation, triggering taxable capital gains. Some gains are exempt, while the tax rate varies by asset type and holding period. It applies to securities, tax-deferred accounts, deferred compensation, and non-grantor trust interests. The US exit tax includes exemptions and deferrals based on net worth, tax compliance etc. For example, some deferred compensation plans such as 401(k) plans are usually not taxed immediately. Instead, these are subject to withholding on future distributions. These provisions offer a certain level of flexibility for those seeking to expatriate.

Balancing Exit Taxes and Global Mobility

Exit taxes are aimed at preventing wealthy individuals and business owners from avoiding taxes by relocating to countries with lower tax rates. Reflecting a broader global trend, countries are tightening tax rules for people relocating abroad. As tax laws evolve, nations want to ensure that people who have benefited from their resources and economy continue to contribute to their domestic tax system, sometimes even after relocating.

The EU has made efforts to curb aggressive tax planning with the Anti-Tax Avoidance Directive, but balancing these regulations with fundamental rights within the EU remains a delicate balance. As member states adjust their exit tax laws, they must comply with EU law while respecting individuals’ freedom of movement within the Union. Ongoing discussions, such as those between the European Commission and Denmark emphasize this fine line.

On a broader stage, global mobility is directly impacted by exit taxes, which restrict relocation options. By imposing exit taxes, countries are increasingly pushing individuals to choose low-tax jurisdictions offering financial incentives to start and scale businesses.

Related Posts

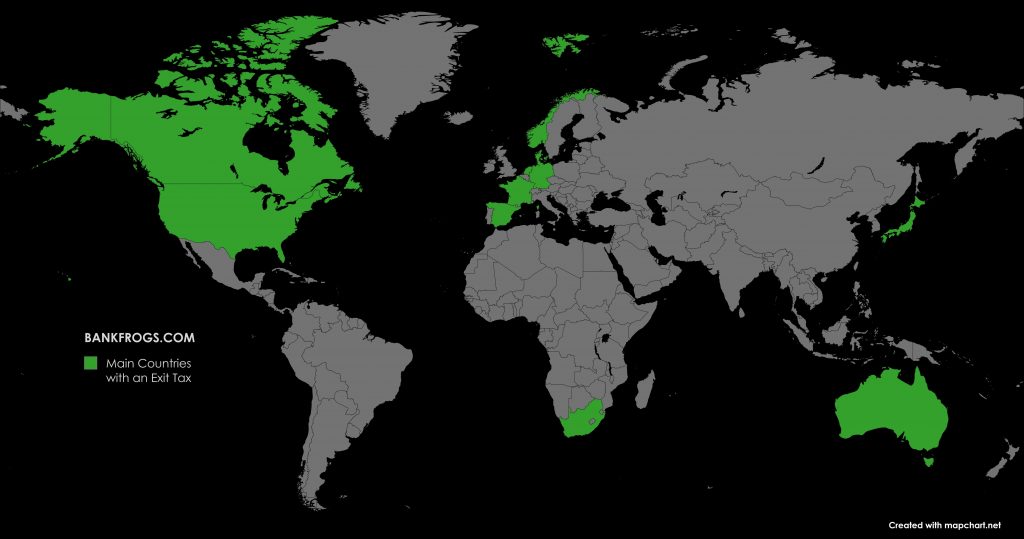

Cover Image: Map of the main countries with an exit tax, created with mapchart.net

References

1. Exchange rates used for the conversion to the United States Dollar are based on data sourced from www.xe.com as of March 9, 2025. Rates used:

- USD 1 = NOK 10.86

- USD 1 = JPY 148

- EUR 1 = USD 1.08

Note: Currency exchange rates fluctuate, and the rates used in this article reflect those available at the time of writing.