Géricault’s painting offers a critique of corruption and incompetence in the French monarchy. It illustrates how government failures brought suffering to ordinary people.

The final decades of the eighteenth century were shaped by revolution on both sides of the Atlantic. In America, thirteen colonies declared independence from Britain in 1776, fighting to establish a republic. In France, the 1789 uprising toppled the monarchy and ushered in a decade of radical political and social change. Despite their different contexts, both revolutions faced a similar financial dilemma:

How could a new government fund itself without an established banking system?

Tax collection was slow, disorganized, and often resisted. Credit was limited and domestic capital markets were weak. Without access to reliable financing, revolutionary governments risked both military defeat and political failure.

The United States and France each took very different approaches to address their financial crises. Alexander Hamilton’s American system aimed to build credibility through debt consolidation and the founding of a national bank. In contrast, Revolutionary France experimented with paper money backed by confiscated Church lands. While Hamilton’s model created the foundation for lasting public credit, the French monetary experiment led to hyperinflation and a collapse of trust in the state, which was only restored later with the creation of a national bank under Napoleon.

US Banking Foundations

The American Revolution revealed just how fragile public finance could be in a young state. In 1776, the Continental Congress declared independence without effective taxing power. The thirteen colonies were loosely united, each guarding their own finances. Congress had no power to tax directly and could only request funds from the states, which often refused. Even the basic medium of exchange was in crisis. Gold and silver coins had always been scarce in the colonies, drained by trade with Britain. Ordinary transactions relied on barter, colonial paper, or bills of exchange. Without hard currency, it was nearly impossible to pay soldiers and suppliers. These circumstances made it difficult to maintain armies in the field

The solution from Congress was the Continental dollar, a paper currency issued in ever-larger amounts, backed only by vague promises of future repayment after victory, possibly through future land sales. At first, the notes circulated out of patriotism and necessity. However, with no tax revenue to back them and inattention from Congress, inflation set in almost immediately.

Robert Morris and the Bank of North America

By 1781, the American fiscal experiment was collapsing, “not worth a Continental” had become a catchphrase for worthless money, soldiers were deserting for lack of pay, and the Revolution risked collapse. In Philadelphia, Robert Morris stepped into the crisis to engineer the Bank of North America as the first credible financial institution in the country. The bank was funded with real gold and silver, some came from Morris’ own assets and that of his commercial network, the rest was mostly borrowed from France. This infusion of money gave the bank a level of trust the Continental Congress could never achieve on its own. Congress granted the bank a public charter, allowing it to operate as a quasi-national institution. Built on that foundation, the Bank of North America began issuing notes redeemable in gold and silver. Unlike the Continental dollar, these notes carried a credible promise of payment. That trust made all the difference for soldiers and merchants who could use the notes at or near face value for daily transactions.

More importantly, the bank also provided short-term credit directly to the Continental Army. Soldiers were paid, suppliers reimbursed, and desertions reduced. What kept the system running was that few were actually paid in coin. Instead, people accepted paper money backed by the bank’s promise. Behind that promise stood Robert Morris himself, often personally guaranteeing the obligations.

However, what kept the revolution alive was foreign loans. France, Spain, and the Dutch Republic extended necessary credit negotiated through a handful of determined American agents. Equally important were private merchants, both American and European, who advanced supplies with no guarantee of being paid back. In effect, the American Revolution for independence and the following years were mainly financed with borrowed money, dependent on outsiders betting that the new republic would survive.

“AT LAST, on June 11, 1782, Adams negotiated with a syndicate of three Amsterdam banking houses […] a loan of 5 million guilders, or $2 million at 5 percent interest. […] It was not the $10 million Congress had expected Henry Laurens to secure, but it was an all-important beginning. It was money desperately needed at home”

Randall Woods, John Quincy Adams [1]

The Bank of North America gradually declined in significance. By the early 1790s, its influence had faded as the newly established First Bank of the United States took over many of its core functions. Although it continued operating for some time, it was eventually absorbed into other banks as the financial system developed.

Silas Deane was an American agent in Paris who played an important role in the American Revolution by securing French aid for the Continental Army.

Hamilton’s Vision for American Credit

When Alexander Hamilton became the first Secretary of the Treasury in 1789, he was determined not to repeat the financial failures of the Revolutionary War. Then in his early 30s, Hamilton had been mentored by Robert Morris who was two decades his senior. Drawing on Morris’ influence and the example of the Bank of England, he understood that public credit depended on discipline, structure, and strong institutions.

Hamilton also looked closely to the writings of Jacques Necker, the Swiss-born banker who had risen to become finance minister of France under Louis XVI. Necker made his fortune in Paris and became a central figure in the financial politics of pre-revolutionary France. His efforts to reform finances through greater transparency and appeals to public confidence left a lasting impression on Hamilton. From Necker, he saw how funded debt could align the interest of creditors to the government’s survival.

Stronger national credit builds trust, and trust attracts investment.

The first problem was to establish American credit, which meant resolving its outstanding debt. In his 1790 Report on Public Credit [2], Alexander Hamilton argued that repaying the debt was essential to earning trust and respect for the new nation.

“That an adequate provision for the support of the Public Credit, is a matter of high importance to the honor and prosperity of the United States.”

Alexander Hamilton, Report on Public Credit [2]

Hamilton’s proposals to Congress were to consolidate state debts under federal control, repay Revolutionary War obligations at full value to build trust, and establish a national bank to anchor the new financial system. The First Bank of the United States, chartered in 1791 with a twenty-year term, brought this vision to life. It was a hybrid institution (part public, part private) which issued notes backed by gold and silver, managed government funds, and helped stabilize the national currency. It also limited the excesses of state banks by offering a reliable alternative to their often unstable paper money.

Yet the bank’s success created political backlash. Critics including Thomas Jefferson and James Madison saw it as a concentration of financial power in the hands of elites which resembled the very hierarchies the Revolution had fought against.

“Hamilton’s plan was characteristically audacious. To an overwhelmingly agricultural country whose citizens were traditionally hostile to banks, he proclaimed that such institutions were “nurseries of national wealth.” To fellow citizens who for the most part viewed government power with suspicion, he proposed a great central bank to facilitate federal financial operations and to bolster and expand the national economy.”

Jacob Cooke, Alexander Hamilton [3]

Banking Crisis and Comeback

Despite its success in stabilizing the young nation’s finances, the First Bank of the United States faced growing political opposition. When its charter came up for renewal in 1811, it failed by just one vote in Congress. Alexander Hamilton had been killed in a duel a few years earlier and many of his longtime critics still held the same views they had two decades before. The concentration of financial power, viewing the Bank as a threat to local control and democratic principles. After it closed, state banks spread rapidly, issuing unreliable paper money and throwing the financial system back into disorder.

The fragility of a fragmented banking system was exposed during the War of 1812. Without a central bank to coordinate funding, the federal government struggled to finance the war effort. By 1814, many state banks had stopped redeeming notes in gold and silver, leaving soldiers unpaid and credit markets paralyzed. Borrowing costs spiked, and the lack of financial structure had real, damaging effects. Even former critics of Hamilton’s First Bank began to acknowledge the foresight behind his vision of a stable, centrally managed financial system.

In response to the financial chaos, Congress chartered the Second Bank of the United States in 1816. Larger, more powerful, and closely modeled on Hamilton’s original vision, it served as the federal government’s fiscal agent, regulated state bank note issuance, and helped stabilize national credit. However, its authority made it a target for political opposition. In the 1830s, President Andrew Jackson launched a highly publicized “Bank War” against it, framing the institution as elitist and unconstitutional. Although the charter expired in 1836, the Second Bank’s two decades of operation demonstrated the lasting strength of Hamilton’s ideas of financial credibility and strong institutions for stable national economy.

Continental Finance

During the Revolutionary War, Congress issued Continental dollars. These quickly lost value. Most of the war was financed through loans from France and the Netherlands, as the US had no central bank to stabilize its finances.

Bank of North America

Robert Morris founded the first national bank to help fund the war. It was weakly capitalized and faced opposition.

Hamilton’s Financial Revolution

Hamilton’s plan focused on funding federal debt, assuming state debts, and creating a national bank to build strong public credit.

First Bank of the United States

The bank issued notes backed by precious metals, stabilized credit, and regulated state banks. Despite its success, the bank faced political opposition, and its twenty-year charter was not renewed. This led to the rise of unstable state banks.

War of 1812 Crisis

Without a central bank, funding the war was chaotic, credit collapsed, and borrowing costs increased dramatically.

Second Bank of the United States

Created to restore order, the Second Bank regulated state banks and stabilized finances. However, it was opposed by Andrew Jackson. The bank charter expired in 1836.

French Revolutionary Banking Without Credibility

If the Americans struggled with too little taxing power, the French had the opposite problem: a powerful centralized state whose financial credibility had collapsed. France entered its revolution burdened by a bankrupt monarchy. Decades of war, royal extravagance, and an inefficient, outdated tax system had drained the treasury. Even earlier efforts at reform by Jacques Necker, the Swiss banker who tried to stabilize public finances, were ignored. By 1789, the monarchy was bankrupt.

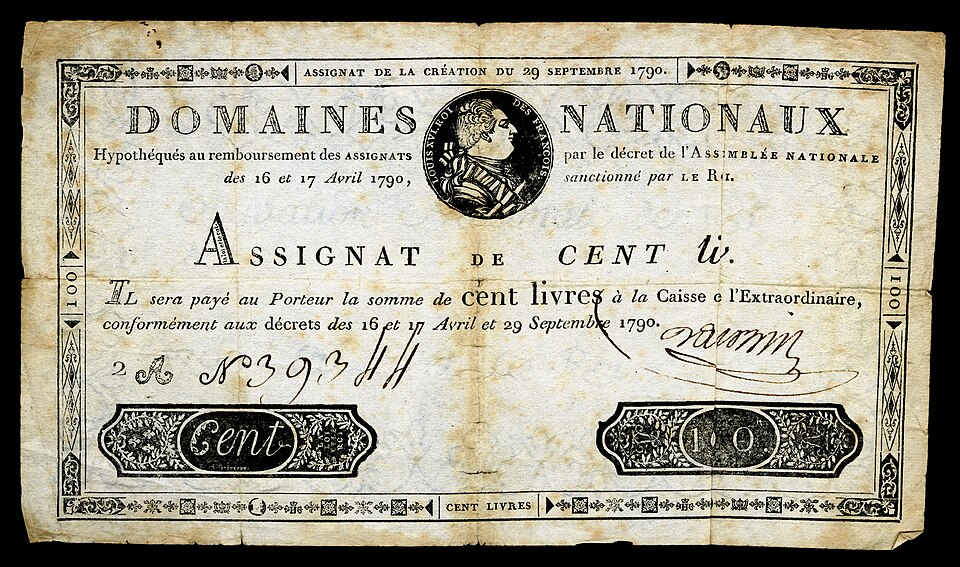

Unlike America, France had a wealth of real assets. In an effort to create liquidity and fund the new government, revolutionary leaders turned to paper money backed by confiscated land (assignats). The Revolution’s most important asset seizure was of church lands (known as biens nationaux or national assets). These were vast estates meant to be sold or used as collateral. Initially intended as interest-bearing instruments redeemable for property, this paper money quickly evolved into a general currency. In theory, the seized land provided France enough wealth to support a new currency. In reality, over issuance of this paper money resulted in high inflation and eroded trust in the system. Adding to the public skepticism, massive royal debts and unstable governments meant that this land-backed paper would remain unreliable.

Existing institutions could not withstand the pressure. Originally created in the 1770s and operating similarly to a modern central bank by influencing interest rates and providing liquidity for the government and merchants, the Caisse d’Escompte became a political tool. Revolutionary leaders debated whether to nationalize it, expand its role, or shut it down entirely. The result was paralysis before its closure in 1793.

As the government shifted from Monarchy to Convention to Directory, each new government brought its own approach to managing money. In 1796, the government tried a second land-backed currency (mandats territoriaux), which turned out even worse than the first. Distrust was so pervasive that citizens began hoarding gold and silver, official markets broke down, and black markets rapidly expanded. Without a central banking authority or disciplined financial institutions, the French revolutionary paper promises were almost immediately discredited, leaving the state unable to mobilize reliable domestic credit.

Napoleon’s Stabilization

The chaos of revolutionary finance was finally brought under control through reform under Napoleon. After the Coup in 1799, the new regime recognized that neither political authority nor military ambition could last without a stable financial system. In 1800, under Napoleon’s guidance, private bankers established the Banque de France. While technically privately owned, it operated in the public interest by issuing notes backed gold and silver reserves in exchange for commercial paper. Unlike the failed assignats and mandats territoriaux, the bank introduced discipline and credibility to the French currency. In 1803, it was granted exclusive rights to issue banknotes in Paris. This was an early move toward a national monopoly. Following a financial crisis in 1805, its governance was restructured under tighter state control, with a governor and two deputy governors appointed by the head of state. With centralized issuance and guaranteed convertibility, the Banque de France built the foundation for stable public credit and restored confidence in both trade and government finance.

Financial Collapse

The monarchy was bankrupt from wars and excessive spending, contributing to the French Revolution.

Nationalization of Church Property

Church lands were seized to back new paper money called assignats, intended as secure notes but soon over-issued.

First Paper Money Experiment: Assignat Inflation and Collapse

Assignats flooded the market, causing hyperinflation and loss of confidence. Gold and silver were hoarded, leading to food shortages and black markets. Assignats became worthless and were abolished in 1796, pushing France back to barter and chaotic local finance.

Second Paper Money Experiment: Short Lived Mandats Territoriaux

Another land-backed paper currency was created but quickly distrusted and collapsed within a year.

Coup of 18 Brumaire

Napoleon seized power, making financial stability a priority.

Banque de France Established

Founded by Napoleon and Parisian bankers, the Banque de France issued notes backed by gold and silver, restoring financial stability, becoming key to the nation’s economy.

Since the adoption of the Euro, the Banque de France no longer issues currency and has had limited monetary power.

Financial Lessons from Two Revolutions

Both the American and French revolutions revealed that political authority alone was not enough to keep armies in the field. Power had to be transformed into financial capacity. To achieve this, each revolution turned to a similar set of financial strategies.

The first was to issue paper claims. Notes, bonds, and bills became promises that future revenues would pay for expenses today. The objective was to convince soldiers and suppliers that these slips of paper had value, even when the outcome of the war was uncertain. The US continued issuing war bonds during major conflicts, especially in the World Wars, and even following 2001 with so-called Patriot Bonds.

Second, they borrowed from foreign lenders. The domestic pools of capital in both countries were either too shallow (in the case of the colonies) or too distrustful (in the case of France). Survival required access to deeper European markets, where merchants and monarchs might gamble on a revolutionary cause in exchange for future repayment or geopolitical advantage. Interestingly, the US struggled to repay its loan from France and defaulted on payments due in 1787. Instead, the US chose to prioritize its Dutch creditors who were seen as the most likely source of new loans. This added to the French financial crisis which played a major role in starting the 1789 French Revolution.

Third, they collateralized their promises. Paper money backed by nothing rapidly loses the confidence of those who hold it. Under the leadership of Alexander Hamilton, the Americans linked future repayment to tariff revenues. This strategy helped build the reputation of US Treasuries, turning them into arguably the safest financial asset of the time. Both revolutions sought to create or reform banking systems to support their goals, yet their implementation and the incentives they produced were different.

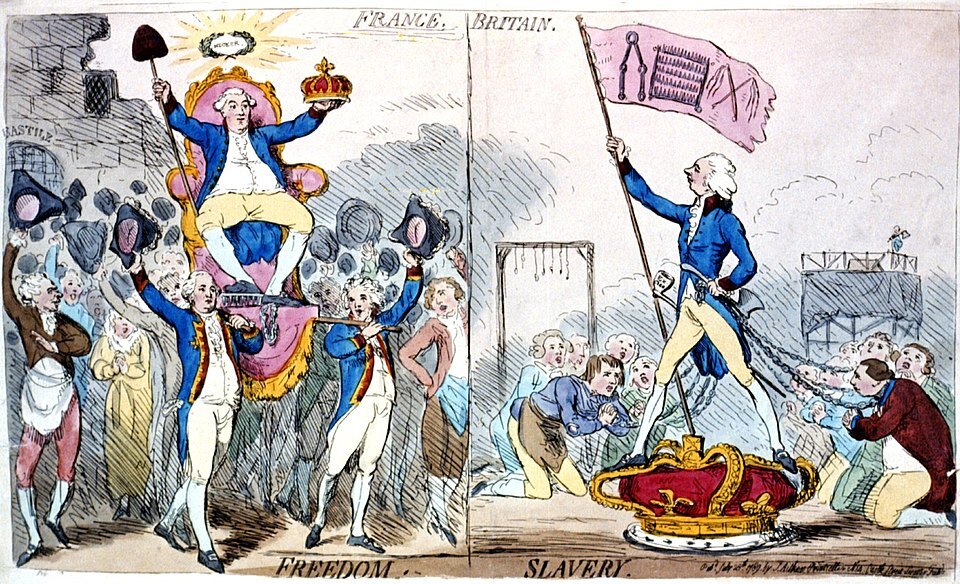

Jacques Necker is triumphing in a land of “Freedom” (France), while on the right, William Pitt represents “Slavery” (Britain). The satirical contrast between French revolutionary ideals and the perceived British repression.

Shared Path to Institutional Credibility

The American and French revolutions illustrate how financial strategy can shape a nation’s future. Both needed to fund armies, support governments, and maintain public trust. However, their approaches to credit were very different. Hamilton’s vision in the United States, inspired by the Bank of England and Necker, built a disciplined system which created lasting financial credibility. In contrast, the use of collateralized paper money in revolutionary France led to inflation and market distrust, leaving the economy fragmented and chaotic.

Yet, in an important convergence, France under Napoleon eventually moved toward the same principles Hamilton had championed. The Banque de France, with its guaranteed convertibility, private participation, and centralized currency issuance, demonstrated that lasting public credit relies on strong institutions, not simply political will. Both nations followed a similar path towards the model pioneered by the Bank of England. Proving that whether in revolution or reconstruction, trust and institutional design are the true foundations of a stable financial system.

Related Posts

References

- Woods, Randall. John Quincy Adams: A Man for the Whole People. Basic Books, 2021.

- Hamilton, Alexander. Report Relative to a Provision for the Support of Public Credit. Treasury Department, 9 Jan. 1790. The Papers of Alexander Hamilton, vol. 6, edited by Harold C. Syrett, Columbia University Press, 1962.

- Cooke, Jacob D. Alexander Hamilton. Macmillan Publishing Co., 1982.