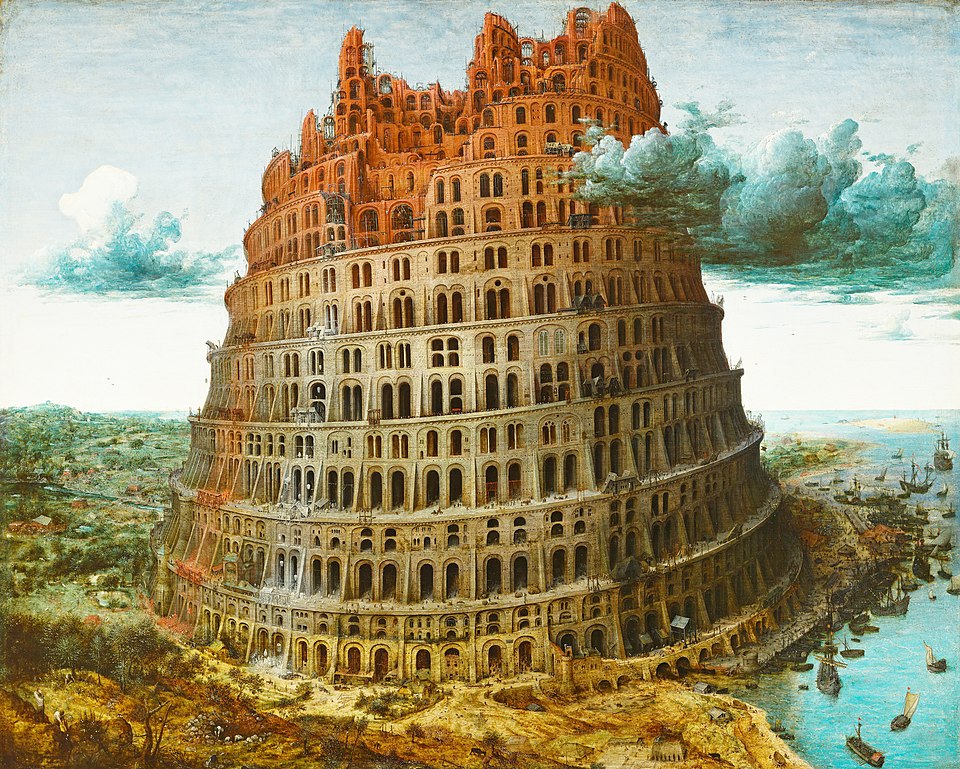

History has always punished excess. Whether in architecture, empire-building, or banking, when growth becomes too much to control, collapse becomes inevitable.

The same pattern repeats itself from money changers in Renaissance Florence to the giants of Wall Street, and even the decentralized cartels of modern narco-economies. Institutions grow to dominate their industry, accumulate resources faster than they can responsibly deploy them, and eventually crumble under the internal weight of their own expansion. As the controversial Jordan Peterson remarked in a lecture connecting the 2008 financial crisis to the Tower of Babel as a symbolic warning structure:

“In 2008, when the politicians said ‘too big to fail,’ […] it should have been ‘so big, it had to fail.’”

The Medici Bank overreach also foreshadowed the excesses of modern financial firms. In 2008, global banks seemed both invincible and dangerously fragile. Even criminal organizations reveal the same structural weakness when scaled. Growth inevitably outpaces control and “too big to fail” has always masked its inverse truth.

Images sources: Commons [1]

Three of the five paintings in Thomas Cole’s series The Course of Empire (1833-1836). It illustrates a cycle of growth leading excess and ending in collapse.

Lessons from the Medici Bank

“[T]he Medici bank was a giant for its time. It may even be argued that it was too large… Rather than refuse deposits, the Medici succumbed to the temptation of seeking an outlet for surplus cash in making dangerous loans to princes.”

Raymond De Roover, The Medici Bank [1]

By the mid-fifteenth century, the Medici Bank had become a major player in the European financial landscape. Multiple branches stretched from Florence to Bruges and London, each run by a trusted junior partner. With money moving across borders and branches reporting back to the main office in Italy, the institution functioned as an early multinational before the term existed.

However, what made the Medici Bank profitable also made it vulnerable. Trade routes were limited and creditworthy borrowers were rare. Rather than turn clients away, the overcapitalized institution began to stretch. Oversight weakened as branch reporting became misleading, and some offices even violated one of the Medici Bank founding principles of never lending to the nobility.

“[the Medici Bank] succumbed to the temptation of seeking an outlet for surplus cash in making dangerous loans.”

Raymond De Roover, The Medici Bank [1]

In many ways, the Medici Bank was the spiritual ancestor of today’s private equity giants. The main firms now sit on mountains of “dry powder,” pressured to deploy capital even when the deals are questionable. Although the form has changed, the tension remains with growth demanding action, even if reckless. Abundance itself can be destabilizing. When success forces you to keep creating, lending, or expanding simply because you can, failure becomes a matter of time.

Medici Bank Leadership Timeline

Modern Capital Surplus

Five centuries later, the same pattern resurfaced on Wall Street and in Silicon Valley. Even though surplus should signal strength, private equity firms today hold trillions in undeployed cash which must be invested to justify management fees and satisfy the expectations of investors.

“Too many dollars chasing too few goods.”

Milton Friedman

Adapted from Milton Friedman’s description of demand-pull inflation, the phrase has been applied to private equity today, with some saying there is “too much money chasing too few good deals.” Such an imbalance creates incentives to deploy cash rather than waiting for better deals. As a result, valuations inflate, due diligence relaxes, and mediocrity starts passing for opportunity. This echoes how the Medici Bank stretched its management, compromising standards and lending to unreliable nobles. Amazon founder Jeff Bezos recently called out the AI bubble, saying:

“Every experiment gets funded. Every company gets funded. The good ideas and the bad ideas. And investors have a hard time in the middle of this excitement, distinguishing between the good ideas and the bad ideas.”

Although his view was ultimately positive, arguing that investing in AI is good for society overall, past bubble bursts have nonetheless disrupted the lives of those involved. For example, the 2008 financial crisis was less a sudden accident than a slow-motion overreach. For years, global banks expanded credit into increasingly fragile structures. Subprime mortgages, collateralized debt obligations, and other instruments were designed to stretch every dollar of capital. The result was an impressive yet fragile tower of leverage built on hollow foundations. When it cracked, it did so exactly as Hemingway writes in his 1926 novel The Sun Also Rises.

‘How did you go bankrupt?’ Bill asked.

Ernest Hemingway, The Sun Also Rises

‘Two ways.’ Mike said. ‘Gradually, and then suddenly.’

We are witnessing the same pattern again today in the credit market. The recent collapses of First Brands and Tricolor revived fears of wider financial stress. Jamie Dimon, chairman and CEO of JPMorgan, warned that “When you see one cockroach, there are probably more,” suggesting that poor lending practices have quietly spread and created hidden risks.

In 2008, financial firms that once appeared unshakable collapsed in a matter of weeks. However, unlike the Medici Bank, these institutions did not disappear as they had grown too big to fail. They were (and still are) so deeply woven into the fabric of the global financial system that their collapse would have brought the entire structure down with them. Since governments could not let the payments system implode, financial support followed. Trillions in emergency liquidity, bailouts, and guarantees were injected to preserve institutions that had outgrown the very rules designed to keep them stable.

Today, banks and financial firms are heavily incentivized to invest. They are guided by the belief that sitting on capital is wasteful and acting on the flawed premise that size is a form of safety. The 2008 collapse of Lehman Brothers nearly froze the global economy, proving that scale has changed the magnitude of consequences, not their nature.

Limits of Franchising

Although growth promises efficiency at scale, that same original efficiency begins to erode once an organization grows past a certain size. The very systems which led to expansion can become too complex to manage from the center. In companies around the world, this often translates into inconsistent standards and damage to brand reputation. Franchising was supposed to solve this problem with a system to expand without centralizing risk. In theory, it allows corporations to replicate success endlessly. Each outlet mirrors the brand, and every franchisee acts as a custodian of the same promise, bound by shared standards. In practice, decentralization trades control for scale. Every local franchise becomes a potential point of failure capable of undermining the entire structure.

Few examples illustrate this better than McDonald’s. In 2015, a customer in Osaka discovered a human tooth in their french fries. As explained in Narconomics [2], it became “a story that made diners around the world think twice about biting into their Big Macs.” Although the incident was isolated, its effects were felt worldwide. Within days, headlines linked McDonald’s to contamination, stock prices dipped, and the company was forced into a public apology campaign. Ironically, McDonald’s operates one of the most rigid franchise systems with standardized procedures, centralized sourcing, and obsessive branding. Yet even that degree of control could not prevent a single lapse from echoing through its global network. One mistake in a local kitchen in Japan triggered reputational damage in markets thousands of miles away.

Even in the corporate world, leaders have long recognized the limits of scale. Jeff Bezos famously introduced the “two-pizza team” rule at Amazon. If a team could not be fed with two pizzas, it was too large to remain effective. When a company grows too large, people lose track of what’s happening, responsibility becomes unclear, and mistakes happen more often. Bezos’ approach is about growing by building small, manageable teams, not by making everything bigger at once.

Size magnifies error. The larger and more decentralized an organization becomes, the more its reputation depends on its weakest link. Franchising creates leverage by expanding with less oversight as each additional layer compounds its weakness. Control is lost with every new branch opening, and no failure is local when a name spans continents.

When the Cartel Franchises

One of my key takeaways from reading Narconomics by Tom Wainwright [2] was discovering that even some parts of the criminal underworld operate similarly to multinational corporations. Over the past decades, major cartels have adopted franchising as their model for expansion. Instead of managing every operation directly, they license their name, supply weapons and know-how, and let local groups operate under their brand. This is the same principle that took McDonald’s global.

At first, the model worked incredibly well. Franchising allowed cartels to expand faster than the state could react. Whether it be Los Zetas, Sinaloa, Guerreros Unidos, a single brand could instantly command fear and recognition. Each local cell paid tribute to the parent organization while diversifying its income. However, the logic of scale once again revealed its limits. As the author explains:

“Franchising overreach has ruined the efficiency of the drug smuggling operation in central Mexico, as rival franchisees spend their time murdering each other (and innocent civilians), rather than getting on with the business of trafficking drugs.”

Tom Wainwright, Narconomics [2]

This has been the case with the Zetas cartel, one of the most infamous adopters of the franchise model. Their decentralized structure led local bosses to become semi-independent warlords focused on their personal power. Each affiliate carried the brand’s power without its discipline, which resulted in the 2011 Zapata incident. US Immigration and Customs Enforcement agent Jaime Zapata was ambushed and killed in Mexico by a local Zetas faction. The killers had mistaken him for a rival trafficker and in doing so, had broken an unwritten rule of the drug trade: never kill Americans, especially not federal agents. In retaliation, the US and Mexican authorities arrested or killed the cartel’s senior leadership within two years.

“Just as a single blunder in a restaurant kitchen can tarnish a company’s global brand, single dire mistake by a group of Zetas affiliates triggered devastating strikes against the cartel’s top leadership.”

Tom Wainwright, Narconomics [2]

The comparison to McDonald’s is almost too perfect since both relied on franchising to expand beyond the limits of direct control, and both suffered brand-level consequences when a single local operation failed catastrophically. Even though franchising allows for rapid spread and brand recognition, it also invites rogue behavior the center can not contain.

Images sources: Commons [2]

Why Big Fails

On one hand, size offers stability by building prestige, raising barriers to entry, and attracting implicit guarantees from clients. The reach of the Medici Bank made it indispensable to the Papal States and Europe’s nobility. Centuries later, the millions of clients served by Citigroup made it indispensable to Washington. Scale creates the illusion of permanence, the comforting belief that something so large can not fail. Yet the same attributes that make an institution formidable also make it weak. Excess capital seeks investment opportunities even when none are safe. Oversight is diluted as hierarchies expand and maintaining returns becomes more important than proper due diligence. The pressure to sustain scale through growth targets, new markets, or simple momentum invites weakness disguised as ambition.

In every age, ambition drives humanity to build higher. Whether it be banks that span continents, corporations that reach every market, networks that bind the world together. Each tower begins with vision and discipline, then grows under the illusion that height equals permanence. This is a recurring pattern of human overreach, the moment when scale outgrows the structures designed to sustain it. We mistake size for resilience, forgetting that beyond a certain point, every empire, institution, or enterprise stops being built on excellence and begins to run on momentum.

2nd Century.

4th Century.

5th Century.

Images sources: Commons [3]

If you want to understand how the balance between money and power started long before Wall Street, read Debt-Run Empires: Why Power Always Defaults Last. From Florentine bankers bankrupted by kings to modern countries trapped in debt cycles, the story of borrowing goes back centuries. The same forces that make today’s banks and states too big to fail once made kings too powerful to pay back what they owed.

Related Posts

References

- De Roover, Raymond. The Medici Bank: Its organization, management, operations, and decline. New York University Press, 1948.

- Wainwright, Tom. Narconomics: How to Run a Drug Cartel. PublicAffairs, 2016.

Images

- Images [1]

- The Savage State (1833-36), by Thomas Cole from Wikimedia Commons.

- The Arcadian or Pastoral State (1833-36), by Thomas Cole from Wikimedia Commons.

- The Consummation (1833-36), by Thomas Cole from Wikimedia Commons.

- Images [2]

- Destruction (1833-36), by Thomas Cole from Wikimedia Commons.

- Desolation (1833-36), by Thomas Cole from Wikimedia Commons.

- Images [3]

- Bust of Marcus Aurelius (2nd Century) from Wikimedia Commons.

- Bust of Constantine the Great (4th Century) from Wikimedia Commons.

- Bust of Leo I the Thracian (5th Century) from Wikimedia Commons.