Swiss banks have long been a preferred destination for individuals seeking to hide assets, particularly due to its strict bank secrecy laws. The Swiss banking system’s reputation for confidentiality made it an attractive choice for US citizens attempting to avoid taxes.

However, in recent decades Switzerland has been at the center of banking scandals. Increased scrutiny from the US government has exposed these practices, particularly regarding tax evasion. As the ties between the US and Switzerland have grown stronger, so too have efforts to clamp down on illicit financial activities involving Swiss banks. For the past few years, major Swiss financial institutions have faced heavy penalties and legal consequences for aiding tax evasion. This is especially true after the implementation of the US Foreign Account Tax Compliance Act (FATCA). Additionally, international agreements to exchange banking information have been introduced to combat money laundering. These changes have fundamentally altered Swiss banking secrecy.

Is Switzerland still the go-to place for hiding assets?

Quick History of Swiss Banking Secrecy

Swiss banking secrecy dates back to the late 19th century, evolving from tradition rather than being codified. Early laws related to bank secrecy were often unclear or limited to certain cantons. Penalties were limited to damages through civil proceedings rather than criminal ones. Despite this, bank secrecy became widely practiced, particularly as Swiss banks sought to attract foreign capital.

In the early 20th century, increased taxation in neighboring European countries led Swiss banks to promote the benefits of banking secrecy to wealthy foreign clients, offering them a refuge from high taxes. Swiss financial institutions launched aggressive marketing campaigns by emphasizing this additional level of protection they could offer. By the end of World War I, Switzerland had transformed into an international financial center. The country was benefiting from international capital inflows, particularly from France, Germany, and Austria.

However, foreign governments, notably France and Belgium, opposed the movement of capital to Switzerland. They feared that it would prevent tax collections and reparations after World War I. These countries sought to force Switzerland into revealing information about account holders. However, the Swiss government resisted and cited the importance of banking secrecy to the domestic economy.

In response to increasing foreign pressure and a banking crises in the early 1930s, Switzerland introduced the 1934 Banking Law. The effect was to formalize and strengthen banking secrecy, notably by making violations a criminal offense. Switzerland became the country with the strongest bank secrecy protections among developed nations.

Recent Swiss Bank Secrecy Scandals

The past few years have seen significant developments in this legal fremework, with prominent Swiss financial institutions facing hefty penalties and legal consequences for facilitating tax evasion. One of the latest cases involved Banque Pictet, a prestigious Swiss private bank which admitted to helping American clients hide $5.6 billion in more than 1,600 secret accounts.

As part of a deferred prosecution agreement with US federal prosecutors, the bank agreed to pay almost $123 million in fines and restitution. This investigation, which stemmed from a 2014 probe, uncovered that between 2008 and 2014, Pictet’s actions helped its US clients avoid paying more than $50 million in taxes. The bank had employed various tactics to facilitate the concealment. This included opening offshore entities, allowing clients to withdraw funds in amounts below the $10,000 reporting threshold for transaction reporting. Among others, it was also offering “hold-mail account services” to obscure account ownership. Pictet has committed to paying nearly $32 million in restitution, a $39 million fine, and forfeiting more than $50 million. The arrangement came with the promise of dismissal of criminal charges after three years if they continue cooperating with investigations.

Hold-Mail Account Services – define

Allows the bank to securely hold account-related mail instead of sending it directly to the client. The purpose is to avoid associating the account with its real owner.

Coded or Numbered Accounts – define

These accounts use a unique code or number instead of the client’s name to guarantee their anonymity.

Shell Entities – define

Legal companies, trusts, or foundations with no real operations, often used to conceal ownership or engage in illegal activities such as money laundering or tax evasion.

The Pictet settlement is part of a broader trend of US efforts to combat tax evasion facilitated by Swiss banks. Credit Suisse, another major Swiss financial institution, was sentenced in 2014 to pay approximately $1.8 billion in penalties after it was found to have helped US taxpayers file false income tax returns. The case was part of a plea agreement that saw Credit Suisse agree to pay a total of $2.6 billion, including $1.8 billion to the US Department of Justice. The bank also faced requirements to disclose its cross-border activities, cooperate with tax information requests, and close accounts of clients failing to meet US tax obligations. Following the announcement of the Swiss Bank Program in 2013, this case signaled the US government’s commitment to eradicating tax evasion, setting a strong precedent for future investigations.

UBS Bubble Bursts and the Collapse of Swiss Bank Secrecy

The first major Swiss bank secrecy scandal was that of UBS AG, Switzerland’s largest bank. UBS admitted to helping US taxpayers conceal accounts from the Internal Revenue Service (IRS). As part of a deferred prosecution agreement, the bank agreed to provide the US government with customer identities and account details. It also agreed to exit the business of assisting US clients with undeclared accounts, and pay $780 million in fines and penalties. UBS had previously conspired to evade IRS reporting requirements, using nominees and shell entities to hide assets. UBS also employed encrypted laptops and counter-surveillance techniques to avoid detection. This agreement marked a significant step in the US Justice Department’s ongoing efforts to combat tax fraud.

Bradley Birkenfeld, a former UBS private banker in Switzerland and a whistleblower, later authored Lucifer’s Banker Uncensored: The Untold Story of How I Destroyed Swiss Bank Secrecy (2016). In his book, Birkenfeld details the strategies the bank used to hide client assets. On page 99[1], he recalls, “My next set of training sessions shattered any notions I might have had that UBS wasn’t up to speed on American tax regulations, or that they didn’t exactly know what Americans could or could not do with their money overseas. In fact, UBS had hundreds of domestic branches all over the States, replete with lawyers and CPAs, so they knew the US banking laws and tax codes upside down and backwards.”

Birkenfeld’s sales pitch to potential clients was simple: “it’s three zeros. Zero income tax, zero capital gains tax, and zero inheritance tax” (page 103)[1].

The author also describes how the bank charged multiple fees for managing and lending clients’ money. The process described in his book follows three main steps:

- Step 1: Management Fee: A 3% annual fee for managing the client’s assets.

- Step 2: Investment in UBS Products: Clients’ funds were invested in UBS proprietary products. These usually carry additional internal fees and potential commissions.

- Step 3: Loaning the Client’s Own Money: UBS used clients’ funds as collateral to lend money back to them, charging interest on these loans.

“UBS was making a fee for holding the guy’s cash in the first place, then making another fee for loaning him his own damn money! And guess what? The guy’s happy! He’s getting his deal done, and he’s still doing it with tax-free cash! I couldn’t believe it, and you know what? It worked, over and over again” (page 99)[1].

Additional details on how illiquid assets are used to borrow money can be found at the end of this article:

End of the Oldest Swiss Bank by FATCA

The increasing crackdown on Swiss banks came along the introduction of the Foreign Account Tax Compliance Act (FATCA) in 2010. The Act requires foreign banks to report information on US account holders to the US IRS. This legislation has made it harder for Swiss banks to maintain their historically secretive practices and has pushed many American taxpayers to come forward and disclose their offshore accounts. The impact of FATCA, along with aggressive prosecutions by US authorities, has sent shockwaves through the Swiss banking system. It signaled a shift in the manner these institutions handle US clients and US tax compliance.

As a result, Swiss banks, once known for their strong privacy protections, are now being forced to adapt to a new era of transparency. Some banks, such as UBS, have avoided guilty pleas by settling for hefty fines. However, Switzerland’s oldest bank, Wegelin & Co., was not so fortunate.

Founded in 1741, Wegelin initially argued it was only subject to Swiss banking laws. The bank eventually pleaded guilty to US charges of helping US taxpayers hide $1.2 billion in offshore accounts. Despite its legal troubles, Wegelin continued to assert its commitment to Swiss banking secrecy. In 2013, it became the first foreign bank to plead guilty to US tax charges, which forced it to shut down. This occurred as FATCA was being fully implemented.

Ongoing investigations into Swiss banking practices reflect the US government’s efforts to combat global tax evasion. As a result, Swiss banks have had to increase compliance with US tax laws. The result has been an increased number of US taxpayers entering voluntary disclosure programs. Meanwhile, bank secrecy, once a cornerstone of Swiss banking, is fading under global financial regulations.

New Developments in US-Swiss Financial Information Exchange

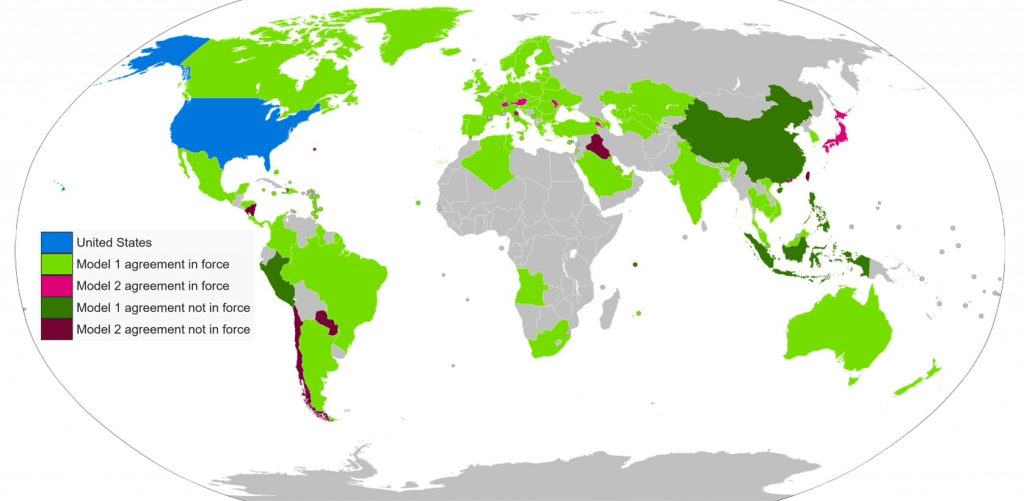

In 2025, Switzerland announced an important change in its FATCA agreement with the US, impacting how financial information is exchanged between the two countries. This shift moves away from the Swiss long-standing bank secrecy tradition and will continue to influence US citizens hiding assets in Swiss accounts. The new agreement is set to take effect in 2027 and will establish a mutual, automatic exchange of tax information.

The Swiss relationship with FATCA dates back to 2014, when the Swiss government signed an intergovernmental agreement with the US under which Swiss financial institutions were required to report US account holders’ financial information to the IRS. Under this agreement, Switzerland adhered to a FATCA Model 2 agreement, which was a unilateral information exchange system. This means that Swiss banks provide account details directly to the IRS, without receiving any information in return.

However, this model creates one-sided transparency to the detriment of Switzerland and its banking system. In response, the Swiss government negotiated a revision to the FATCA agreement. Under this new FATCA Model 1 agreement, both Switzerland and the US will automatically exchange account information. The revised agreement negotiated in November 2023 is expected to take effect at the beginning of 2027.

The Federal Palace of Switzerland in Bern houses the Swiss government’s legislative and executive bodies and serves as a center for political decision-making.

Impact on US Citizens with Swiss Accounts

The new FATCA agreement is part of broader global efforts to combat tax evasion and increase transparency in cross-border financial transactions. In fact, it was introduced after the adoption of automatic tax information exchange under an OECD-developed multilateral agreement.

However, despite these global moves toward transparency, certain jurisdictions continue to exploit loopholes. The US state of Delaware, for example, remains one of the largest tax havens for foreigners, as detailed by Oliver Bullough in his book Moneyland: How Thieves and Crooks Now Rule the World (2018). Its lax corporate tax laws and the ability to register companies anonymously have made it an attractive alternative to traditional banking secrecy. Effectively allowing entities to hide their true ownership.

This practice was nearly ended by the Corporate Transparency Act implemented in 2024. However, since its introduction, legislators have significantly reduced the scope of the Act.

The Next Frontier in Hiding Assets

Sharing a frontier with Switzerland, Liechtenstein is mentioned in Birkenfeld’s book as an increasingly popular alternative to Switzerland for those seeking to hide assets from tax authorities. While Swiss bank secrecy once set the standard, Liechtenstein has raised the bar even further. As the insider notes, in Liechtenstein the “banking laws were even more covert and rock-solid than in Switzerland” (page 146[1]).

The appeal of Liechtenstein lies not only in its solid banking secrecy, but also in its ability to offer more complex structures to hide assets. Specialized lawyers, accountants, and professional trustees all work together to hide assets. Intricate networks of legal structures create distance between the true owner and their possessions. The author advised a client:

“Then I’m going to refer you to a close friend of mine, a savvy CPA and trustee in Liechtenstein. That gentleman will set up company structures, trusts, foundations, and so forth. Your name won’t appear on any of their records, but you’ll be the ultimate beneficiary” (page 85[1]). Moreover, the bank secrecy culture in Liechtenstein has made it a tax haven. The country has become a top choice for those seeking to keep assets hidden from tax authorities.

The book tells the story of Igor Olenicoff. A Billionaire who chose to move his funds from UBS to a smaller, more discreet bank in Liechtenstein. He believed that “the Liechtensteinians were even tougher than the Swiss when it came to outsiders screwing with their private business” (page 148[1]). This sentiment is echoed in the official 2008 Department of Justice press release. It revealed how certain clients were advised to misrepresent funds as loans. Others were instructed to destroy offshore banking records and file false tax returns to conceal their wealth. As global attention on tax evasion grows, individuals trying to hide assets are turning to regions with more secretive banking systems.

“Some tax havens are little-known places like Andorra and Vanuatu that few Americans have heard of. Others, like Switzerland and Liechtenstein, are notorious for operating behind a ring of secrecy. Billions and billions of dollars’ worth of US assets find their way into these secrecy tax havens.” (page 285[1]).

End of an Era

Switzerland was once renowned for its ability to hide assets. As a series of high-profile scandals have since come to light, this long-standing reputation as a secretive tax haven is no longer holding true. The implementation of FATCA and international transparency agreements has forced important transformations in the Swiss banking system. The shift from bank secrecy to greater openness marks a fundamental change in the manner Swiss financial institutions operate. While Switzerland remains a key player in global finance, the landscape is evolving. Those seeking to hide assets can no longer rely on the same level of protection. As global efforts to combat tax evasion and money laundering increase, Switzerland’s role in facilitating asset concealment continues to fade away.

Related Posts

References

- Birkenfeld, Bradley. Lucifer’s Banker Uncensored: The Untold Story of How I Destroyed Swiss Bank Secrecy. Greenleaf Book Group Press, 2016.

- Bullough, Oliver. Moneyland: The Inside Story of the Crooks and Kleptocrats Who Rule the World. St. Martin’s Press, 2018.