The Allure of Quick Cash

Imagine being your own boss, no manager, no 9-to-5, just freedom and financial independence. It’s a seductive promise, and it’s exactly what draws millions into business models that blur the line between entrepreneurship and exploitation.

From multi-level marketing to so-called “gifting circles” and overhyped investment, the common thread is powerful: financial incentives that reward belief more than results. The promise of easy money often overshadows the reality beneath it.

The psychology and mechanics behind these models reveal a thin, often invisible line between genuine opportunity and calculated manipulation. In a system built on hype, recognizing that difference can mean the distinction between building something real, or getting played.

MLM Selling the Illusion of Entrepreneurship

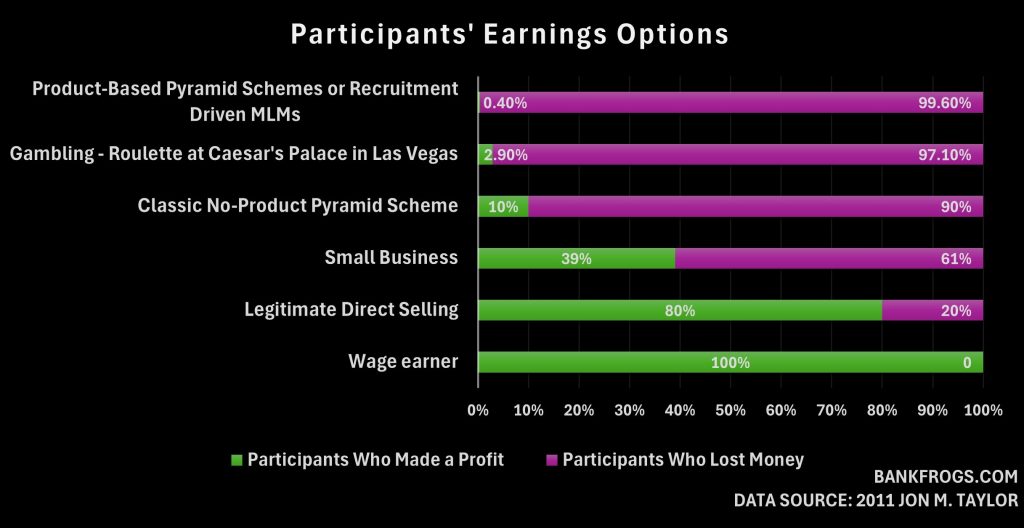

Multi-Level Marketing (MLM) is often sold as the ultimate path to financial freedom. The pitch is familiar: “Be your own boss,” “Work on your own terms,” and “Earn unlimited income.” On the surface, it sounds like a classic entrepreneurial model. You sell a product, build a team, and be compensated for both. In reality, MLMs often rely more on recruitment-driven financial incentives than genuine product sales.

In an MLM, you can make money by selling products and by recruiting others into the business. But the reality is that the compensation structure heavily favors recruitment over sales. While the model is framed as building a team or “sales organization,” those who focus on bringing in new members often earn far more than those who focus on actual product sales.

Financial Incentive Trap

Although the model promotes the dream of upward mobility, in reality, that dream is statistically out of reach. The vast majority of MLM participants never make a profit and actually lose money once starter kit costs, event fees, and personal inventory purchases are factored in. Meanwhile, those at the top profit handsomely, but not by selling products themselves. Instead, they building massive referral pipelines of new recruits (called downlines) beneath them in the hierarchy.

This creates a distorted system where success depends less on selling a product and more on how many people you can recruit. Some of the most telling red flags include:

- An emphasis on recruiting over product sales

- High upfront costs to “join” or get started

- Promises of passive income with minimal effort

The result? A structure that rewards recruitment while disguising itself as retail.

“This newly created equity would be based on the only true currency known in the sales managers’ world, the labor and expenditures of recruited sales people. The real commodity to be marketed under the new plan […] would be the salespeople themselves. The clay of the sales managers’ craft.”

Robert FitzPatrick in Ponzinomics [1]

Where MLM Ends and Pyramid Schemes Begin

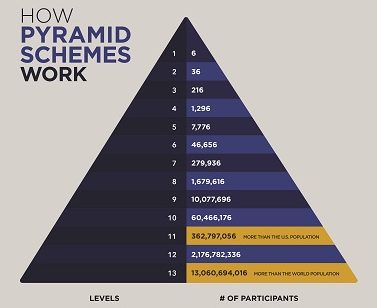

At a certain point, the line between MLM and pyramid scheme becomes so thin it is almost meaningless. A pyramid scheme takes the MLM model to its logical extreme by removing the product entirely. Participants make money solely by recruiting others, who pay to join and are encouraged to do the same. Money flows upward to earlier participants, not from customer demand, but from a constant churn of new people buying in. This structure depends on constant exponential growth leading to inevitable collapse.

These schemes are often disguised with clever branding and buzzwords including “gifting circles,” “abundance fractals,” “crowdfunding communities”. Regardless, the mechanics are the same: get in early, bring in others, and cash out before the whole thing collapses.

The key difference comes down to values. MLMs disguise themselves as businesses that sell products, all while profiting from recruitment. Pyramid schemes don’t even pretend. In both cases, those at the bottom pay the price.

What these systems really are is a funnel of false hope, where financial losses are masked by motivational rhetoric, and personal failure is blamed on lack of effort, not a broken system. At their core, both models sell an idea of wealth built not on value creation, but on access, your ability to recruit, persuade, and pull others into the same system.

Although often confused, Ponzi schemes and pyramid schemes are different types of investment fraud. Ponzi schemes pay earlier investors using money from new investors, without real profits, while pyramid schemes rely mainly on recruiting new participants to reward those above them.

Pyramid Schemes Psychological Tactics

Beyond the faulty economics, pyramid schemes often rely on strong emotional manipulation. Participants are encouraged to adopt cult-like loyalty, where questioning the model is discouraged and leaving the group is seen as failure. Social pressure, motivational hype, and even spiritual language are used to keep people invested emotionally and financially.

When Financial Incentives Blur the Line

Taking the example of financial instruments, while annuities and Indexed Universal Life (IUL) insurance policies are not technically MLM products, they are often sold using similarly aggressive, commission-heavy tactics. These products, complex by design, are marketed through networks of independent agents. Many of whom operate under what looks and feels like a multi-tiered sales structure.

Although it is not a formal MLM, the financial incentives often mirror one. Agents are encouraged not only to sell but also to recruit others beneath them, earning override commissions on the sales those recruits generate. The result is a system where the quality of financial advice can quickly become secondary to sales volume. The formula is simple:

More recruiting = more commissions.

More commissions = more pressure to sell, not advise.

This dynamic turns financial guidance into a numbers game. Success and income is tied not to client outcomes, but to how many policies you can move and how many people you can bring into the fold. And when the products involve long-term contracts and high fees (as is often the case with annuities and IULs) the cost of bad advice falls on the consumer.

Guaranteed Income or Golden Handcuffs?

Annuities are often marketed as the solution to one of retirement’s biggest fears: outliving your money. In simple terms, you trade a lump sum today for a guaranteed stream of income in the future. On the surface, it sounds like peace of mind.

Broadly speaking, annuities fall into categories such as fixed or variable, based on whether payouts are predictable or tied to market performance. They are attractive to those concerned about outliving their savings. But that security does not come without trade-offs. Annuities often carry high fees, surrender charges for early withdrawals, and limited liquidity, meaning investors may be unable to access their money when they need it most. In addition, the opportunity cost of locking up funds in a conservative product may mean missing out on greater growth elsewhere.

Selling Safety, Delivering Complexity

To be clear, annuities are not inherently unethical. In the right situations, especially for the ultra-wealthy, they can be a useful financial tool. High-net-worth individuals with plenty of liquidity may use annuities as part of complex estate planning strategies.

However, those strategies are often simplified, repackaged, and used as justification for annuities to be aggressively marketed to everyday investors. As if they were a fit for everyone, often without enough explanation of the trade-offs involved. Their long-term horizon and limited liquidity can become real obstacles for people who might need more flexibility, are carrying debt, or don’t have much savings to begin with.

This is a good example of how financial strategies that work well at the top end of the wealth spectrum do not always translate further down. Regular investors may become locked into something they can not afford to get out of.

Protection or Profit?

Similarly to annuities, life insurance is often sold under the banner of financial security, with an underlying sales model driven by commissions. Agents earn more by selling higher-cost products, especially whole life insurance, which is frequently pushed over simpler, more affordable term policies.

While whole life has its place in long-term wealth strategies, it is often marketed as a one-size-fits-all solution regardless of the actual needs. Add-on riders and investment promises can inflate costs without offering real value. All of which blur the line between advice and upsell. The question becomes: Is this policy about protection or hitting quotas?

Once again, the insurance world is not inherently unethical, but financial incentives make it full of gray areas.

Pyramidal structures, found across the globe in civilizations with no known contact, appear to reflect a universal architectural pattern in human development.

Navigating the Financial Incentive Minefield

In a world saturated with polished sales pitches and promises of passive income, it is easy to get lured into financial models that appear to be opportunities but turn out to be traps. From commission-heavy products to MLMs disguised as entrepreneurship, and even outright pyramid schemes, the common thread is the same: a business built more on belief and recruitment than real value.

If it sounds too good to be true, it probably is.

In today’s financial landscape, your best defense is financial literacy. Understanding how these systems operate, the financial incentives behind them, and who truly profits, are the keys to making informed decisions.

Take a critical look at what you are investing in. Ask the uncomfortable questions, and don’t confuse a motivational message with a good investment. Real opportunity is built on transparency, not hype.

Related Posts

Cover image: Pyramids of Giza in Egypt (2016), Commons

Reference

- FitzPatrick, Robert L. Ponzinomics: The Untold Story of Multi-Level Marketing.

Mosaic Press, 2019.