Every empire runs on borrowed money, the only question is who gets to pretend they will pay it back?

After having crowned himself, Napoleon stands ready to crown Josephine as the first Empress of the French.

Debt has always been the quiet language of power, and every empire borrows its strength through it. Every system built on debt begins as a story of trust and ends as a test of who can survive its collapse. From Florence to Washington, those who seem safest are often those who can not afford to be doubted, and those who demand repayment rarely hold the means to enforce it. Debt is a weapon of the powerful, a way to command resources without surrendering sovereignty. From their mistakes, the Florentines learnt that money lent to power is rarely returned. Yet centuries later, lenders still queue for the privilege. Calling it sovereign debt, they trust that rulers, corporations, and nations will honor debt promises.

This is the story of how debt became the architecture of authority, the hidden scaffolding of empires, markets, and modern institutions built on the illusion that numbers on paper mean control.

The Bardi and Peruzzi Bankruptcies

In early Renaissance Europe, money and power were two sides of the same coin. To lend to a king was to buy influence with inner circle favors and a front-row seat to his campaigns. The profits, if they ever came, were almost secondary.

For the bankers of medieval Florence, lending to a king was the ultimate status symbol, and the fastest road to bankruptcy. The Bardi and the Peruzzi learned that lesson the hard way in the 1340s. Two of the mightiest banking families in Florence lent vast sums to Edward III of England, funding his conflict against France which became the Hundred Years’ War. No merchant could rival the prestige of financing a monarch’s war. The bankers soon realized they had gone too far. Yet they kept lending to protect earlier loans and to secure access to the lucrative English wool trade. With no quick victory in sight, Edward III simply defaulted in 1343. He owed 900,000 gold florins to the Bardi and 600,000 to the Peruzzi, none of it ever repaid. Both houses collapsed, taking with them the savings from wealthy individuals throughout the Italian city-states.

Extending credit to Edward III had been a high-stakes gamble dressed up as a royal partnership. When the king defaulted, Florence paid the price. Future bankers would remember the lesson.

A prince never lacks legitimate reasons to break his promise.

Niccolò Machiavelli, The Prince

Learning from Collapse

After the collapse, smaller banks survived and by the end of the century some had emerged as major financial powers. Amongst them were the Medici, who learned the lesson without abandoning the game. Rather than lend to monarchs, they vowed never to finance nobles [1] and instead backed the papacy, an institution too holy to default. The Church, in need of constant funds to maintain the Papal States, became a perfect borrower, wealthy, influential, and most importantly, immortal.

This shift turned the Medici from moneychangers into monarchs of another sort. By attaching themselves to religion instead of royalty, they aligned debt with a certain divine legitimacy. In theory, they were hedging their risk with a spiritual guarantee of repayment.

Prestige remained the riskiest kind of collateral since lending to the powerful meant accepting that repayment was uncertain. Beyond a potential income, the real return was the influence these loans brought. During this period, the closer you were to power, the less likely you were to see your money again.

The Medici thrived because they understood that banking was as much about maintaining relationships as managing money. They perfected the art of selective blindness by funding prestigious clients to increase their own status while hiding the weakness of the system. By lending to an institution deemed too big to fail, they played into the illusion that some debtors are simply too important to default. It would not be the last time history rewarded the debtor over the creditor.

The Noble Art of Default

In the hands of the powerful, defaulting is simply negotiation. For a medieval peasants or merchants, non-payment resulted in ruin. For monarchs with leverage, it was an instrument of statecraft.

No one perfected this art quite like Philip II of Spain, remembered by as the borrower from hell. Between 1557 and 1596, he defaulted four times, bankrupting the most prestigious financiers in Europe. Among them were the Fuggers, who had bankrolled emperors, and the Genoese merchant-bankers, who tried to replace them. Each time, Philip declared a “payment suspension,” blamed divine providence or administrative confusion, and demanded renegotiation. [2]

Spain was a European superpower, holding large amounts of New World silver, commanding fleets, armies, and colonies. It gave the illusion of being the richest empire on Earth while being a debtor empire, bleeding cash through endless wars and religious crusades. The more the empire expanded, the faster it went broke. And yet it worked. Each default ruined a few banks, but credit always returned. The Genoese lent again and the Germans forgave. Although Lenders knew Philip might never repay them, what they truly feared was the cost of being shut out of Spain’s business.

Philip II made himself too essential to challenge and could outlast his creditors. Today, economists would call it systemic importance.

“Genoese lenders’ indulgence of Philip II of Spain’s expensive taste for warfare caused not only the first sovereign bankruptcy in 1557, but the second, third and fourth as well.”

Drelichman & Voth, Lending to the Borrower from Hell, quoting The Economist.

The Danish king Valdemar IV conquered Gotland and ransomed Visby’s merchants to save their city.

The Sovereign Advantage

Philip II understood that the power of a debtor grows with the number of creditors. Once enough people rely on your solvency, they will do anything to preserve the illusion. The same logic has remained for centuries.

- Then, the richest clients (kings, emperors, popes) were the riskiest borrowers.

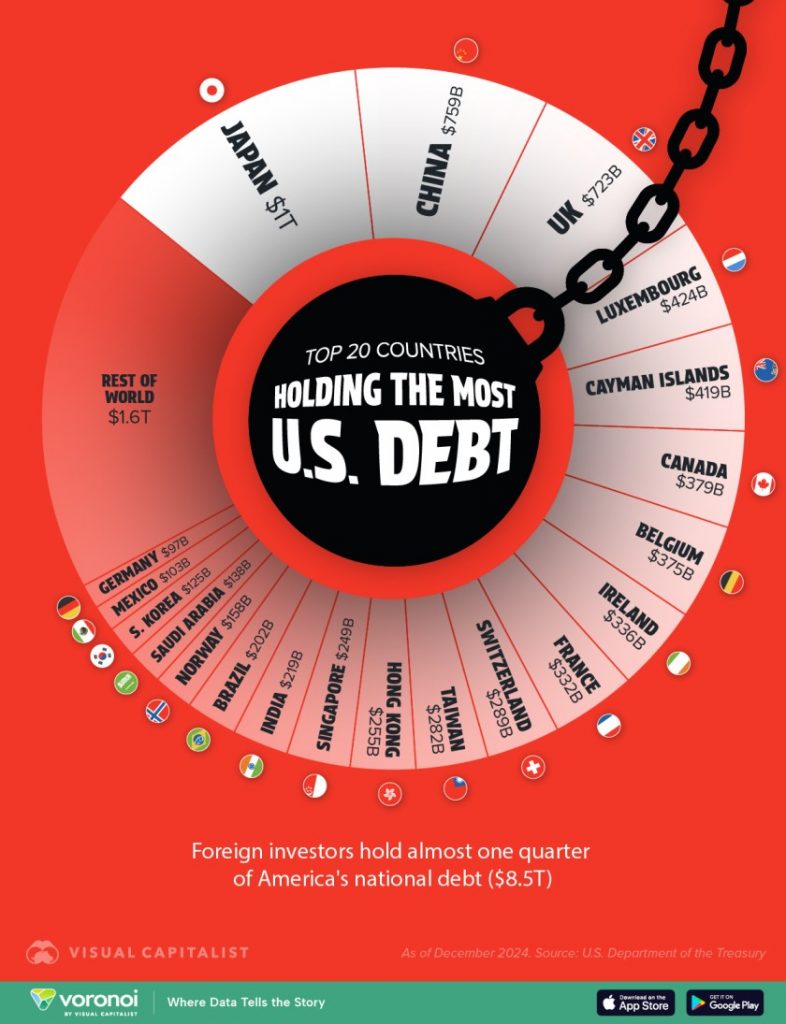

- Now, the richest nations (the US, Japan, China) are seen as risk-free, precisely because default is unthinkable.

However, the illusion remains the same with sovereign credit no longer backed by gold but by trust in its repayment. The belief that treasuries will roll over their debt forever and that markets will always believe they can. In many ways, the bond market is simply the modern version of the court of Philip II. That being a procession of lenders who know the risks, but can not afford to walk away.

In Game of Thrones, the Iron Bank of Braavos mainly lends to governments, military leaders and, and other banks. Yet even the Iron Bank hesitates to collect from the powerful until it can bet on a stronger successor. Creditors do not call in a debt they are not able to enforce. Believing that reputation, not repayment, maintains power has built empires on the myth of solvency.

From the Spanish defaults to the modern crises of Greece, Argentina, and Sri Lanka, the common pattern is one of forgiveness. Default is never the end of the system, it simply resets the scoreboard without admitting that the game is rigged. Each collapse clears the field for new lenders, new narratives and new illusions of repayment. By the late Renaissance, bankers had learned to stop lending to nobles. The next evolution of credit left monarchs behind and replaced them with faceless institutions and markets just as capable of ruin.

Louis XIV is represented as a triumphant ruler bringing stability to the French treasury, next to the personifications of Finance and Abundance. Around them, disorder and corruption are banished.

From Monarchs to Nation-States

The same logic which once allowed kings to default without consequence can now be found in modern economies. Prestige still shields the powerful from being accountable.

By the 18th century, royal debt had evolved into sovereign bonds, a cleaner, more institutionalized form of the same bargain. Kings had to ask for loans while states now issued legitimate promises on paper. This innovation separated the debt from the debtor as a monarch could die, but a nation could live on, rolling over obligations indefinitely. The state has become a perpetual borrower that never technically defaults.

The Bank of Amsterdam pioneered the model of government finance based on credibility and institutionalized public debt, and Britain perfected it after 1694. Founded to finance government wars, the Bank of England rapidly became a cornerstone of the British Empire. We now treat the bonds of wealthy nations as sacred instruments backed by inertia. If markets believe the US, Japan or the Eurozone will keep rolling over their debt, the magic holds. Yet a Greek crisis, a debt-ceiling showdown or a credit downgrade occasionally pull back the curtain, revealing that the powerful debtor is still running the show.

Oligarchs, sovereign wealth funds, and politically exposed persons (PEPs) are now part of the new royalty, occupying the same ambiguous territory once held by monarchs. Financial institutions scrutinize these accounts and their transfers closely, all the while hoping the client’s reputation holds. As with medieval kings, clients offering the most prestige often carry the greatest risk. This underlying tension has created the wave of debanking controversies seen today.

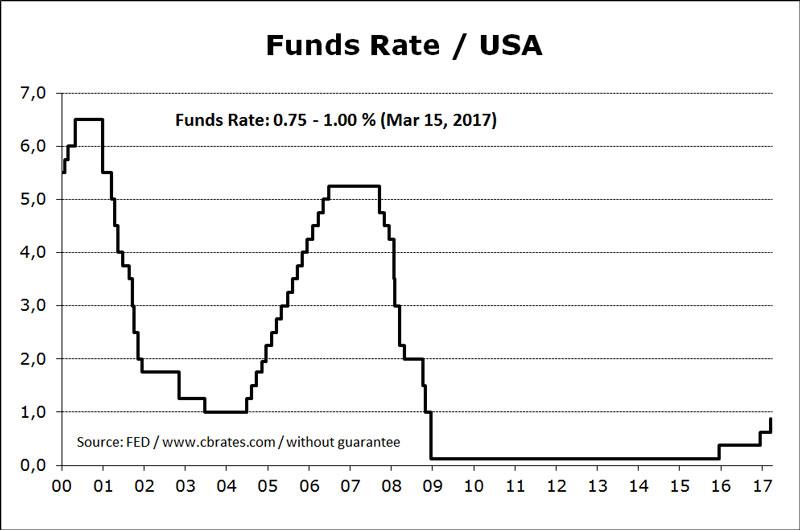

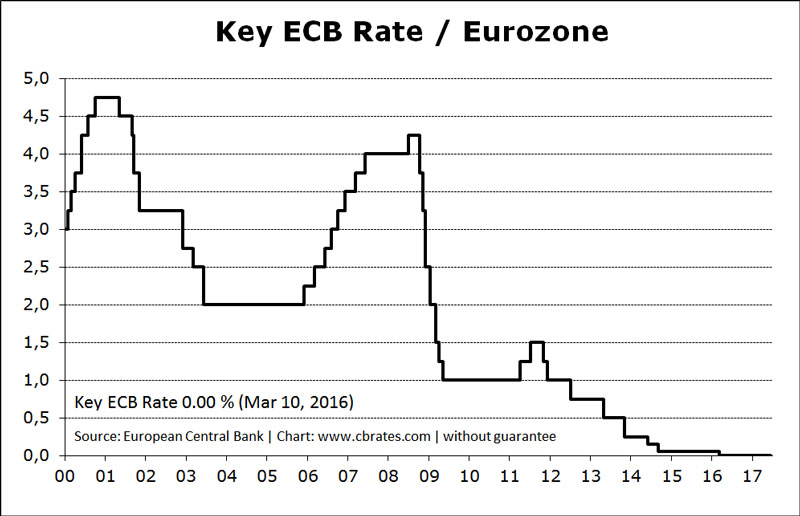

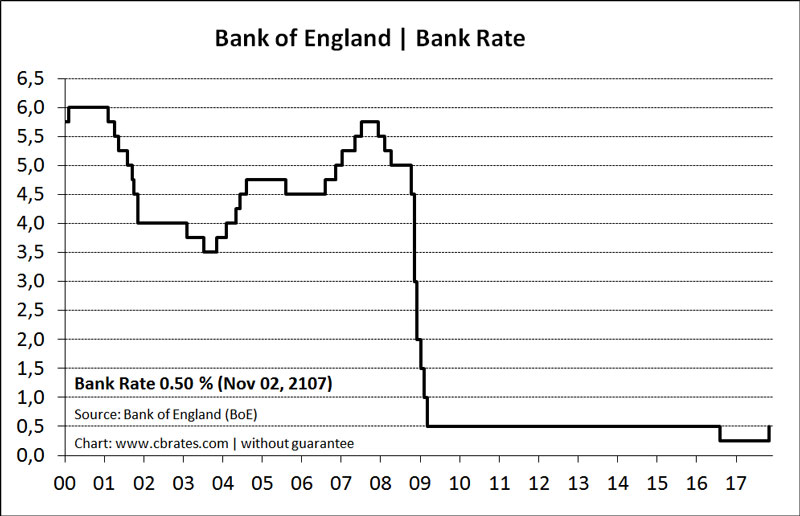

Charts illustrating the evolution of central bank interest rates over time for the Bank of England, the US Federal Reserve, and the European Central Bank. All three show periods of economic intervention, including the era of Zero Interest Rate Policy (ZIRP), where rates were kept near zero to stimulate growth during financial crises.

Charts from cbrates.com

Sharks Can Not Stop Swimming

Debt is not a static instrument, it is in constant motion. Like a shark, it dies if it stops moving. When debt repayments stop or liquidity dries up, the system suffocates. Unlike equity, debt must flow, rollover, and compound. The shark does not rest, and neither does leverage.

Following the 2008 financial crisis, central banks introduced Zero Interest Rate Policies (ZIRP) and massive programs of quantitative easing. Cheap money was everywhere. Governments and corporations gorged on leverage to refinance the old with the new instead of investing efficiently. Motion became the substitute for solvency as debt was rolled over indefinitely, regardless of cash flow. A global culture of credit emerged in which moving money was proof of repayment. The shark swam faster, and the world applauded its speed.

That era has now ended. Central banks have raised rates, liquidity is tightening, and the illusion of perpetual solvency is challenged. Refinancing is no longer free and old debts now demand real attention. Borrowers who once relied on motion must now repay, restructure or default on their debt.

Debt in motion extends to geopolitics as is the case with the interdependence of major powers. The US needs China to hold Treasury bills, China needs US dollars to maintain its reserves. Neither can pull the plug without self-harm. In effect, we have mutually assured financial destruction. Debt in motion maintains the illusion of stability the geopolitical order. Everything works until someone finally calls the bluff.

Illusion of Safety

Since debt and power rarely coexist peacefully for long, the cycle always repeats. Lenders, seduced by prestige and gain ignore the risks until it becomes too late. The Bardi and Peruzzi banks collapsed under the wars of Edward III. Later, the Fuggers were undone by the repeated defaults of Philip II. Today, the risk is broader and harder to see. Banks and bondholders continue to finance sovereigns considered “too big to fail,” nations whose political and economic weight leaves lenders little choice but to comply.

The so-called risk-free rate at the heart of modern finance is a collective fiction. Governments are seen as infallible and their sovereign debt as safe because everyone agrees to pretend they are. When belief itself is the collateral, even a modest downgrade or liquidity crisis can expose the illusion supporting trillions in interconnected debts.

Politics of Default

Debt has always been less about repayment than hierarchy, influence, and survival. The same system that let the Medici prosper, Philip II weaponize default, and modern sovereigns to roll over trillions is still governed by those who can afford not to pay. From Florence to Frankfurt, Wall Street to Beijing, every creditor who forgets this ends up in the graveyard of lenders. Prestige, motion and illusion may keep the system afloat, but power decides who sinks.

Related Posts

References

- De Roover, Raymond. The Medici Bank: Its organization, management, operations, and decline. New York University Press, 1948.

- Drelichman, Mauricio, and Hans-Joachim Voth. Lending to the Borrower from Hell: Debt, Taxes, and Default in the Age of Philip II, 1556–1598. Princeton University Press, 2014.